IFRS 9-ECL

Expected Credit Loss Engine

End-to-end platform for portfolio assessment, model development, ECL calculation, and regulatory reporting — fully compliant with IFRS 9, Basel III, and local central bank requirements.

Stage Assessments

Calculation Methods

Model Studio Tabs

Report Templates

Calculate. Govern. Report — ECL with confidence.

The IFRS 9-ECL Platform

All modules working in concert — an animated tour of your unified platform

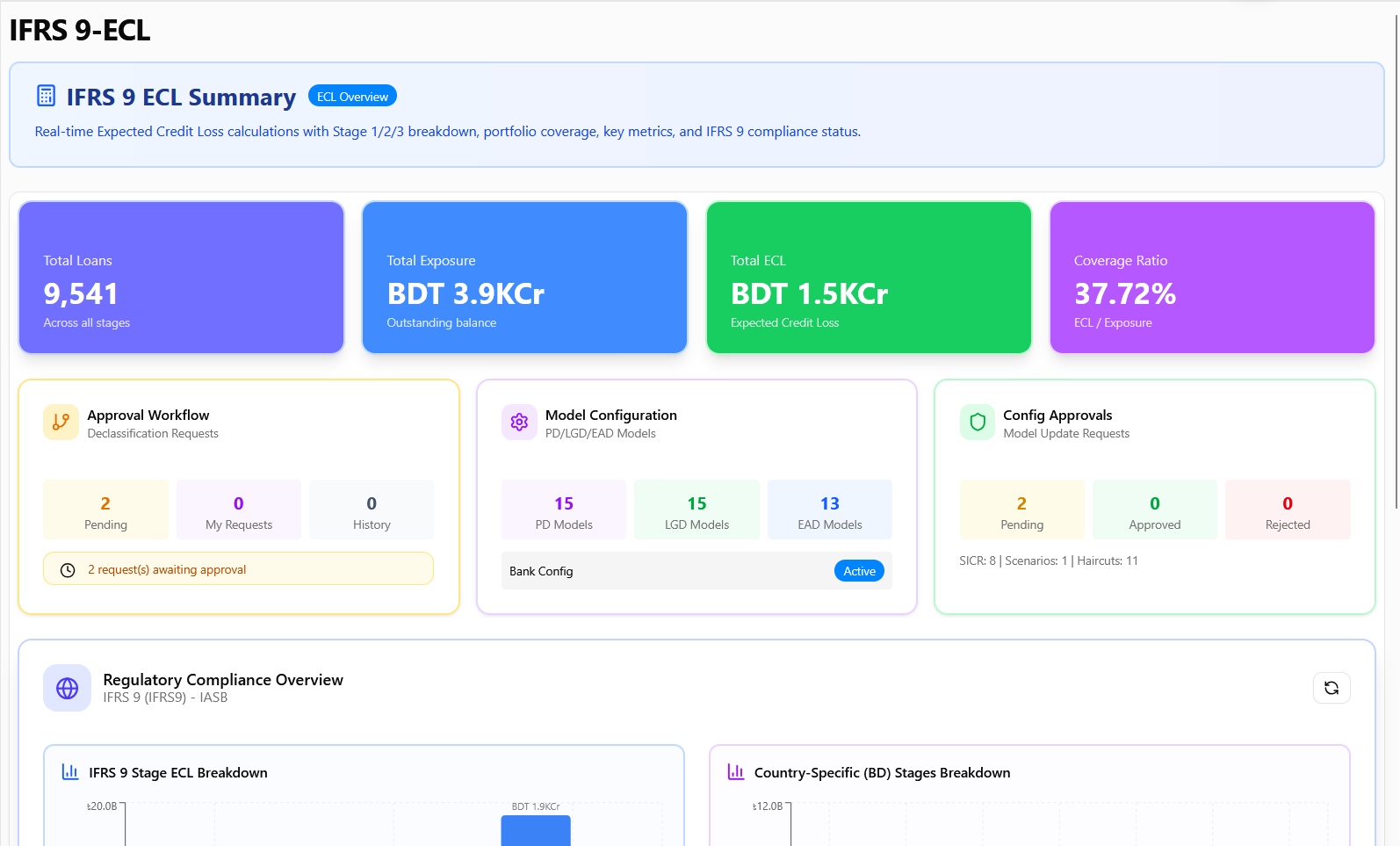

Portfolio Assessment

End-to-End in Five Modes

The platform operates across five integrated modes — from data intake through regulatory filing — each serving different user groups and use cases.

Portfolio Assessment

Guided 7-step wizard transforms CBS data into auditable risk parameters with SICR evaluation, DPD analysis, scenario modeling, and ML-driven recommendations.

Model Studio

Unified workspace for PD, LGD, EAD, SICR, Macro, Collateral, and CCF configuration — with version control, 4-eye approval, and full audit trail.

ECL Calculation

Four calculation methods (Standard, Simplified, Monte Carlo, Advanced) with scenario weighting, discount factors, and batch processing for 100K+ exposures.

ECL Analytics

Real-time dashboards with stage migration analysis, sensitivity analysis, backtesting, cashflow timelines, and run comparison for board-level reporting.

Analytics & Audit Trails

Immutable audit trail with cryptographic chaining, 9-dimension ML recommendations engine, regulatory compliance mapping, and complete chain-of-custody logging.

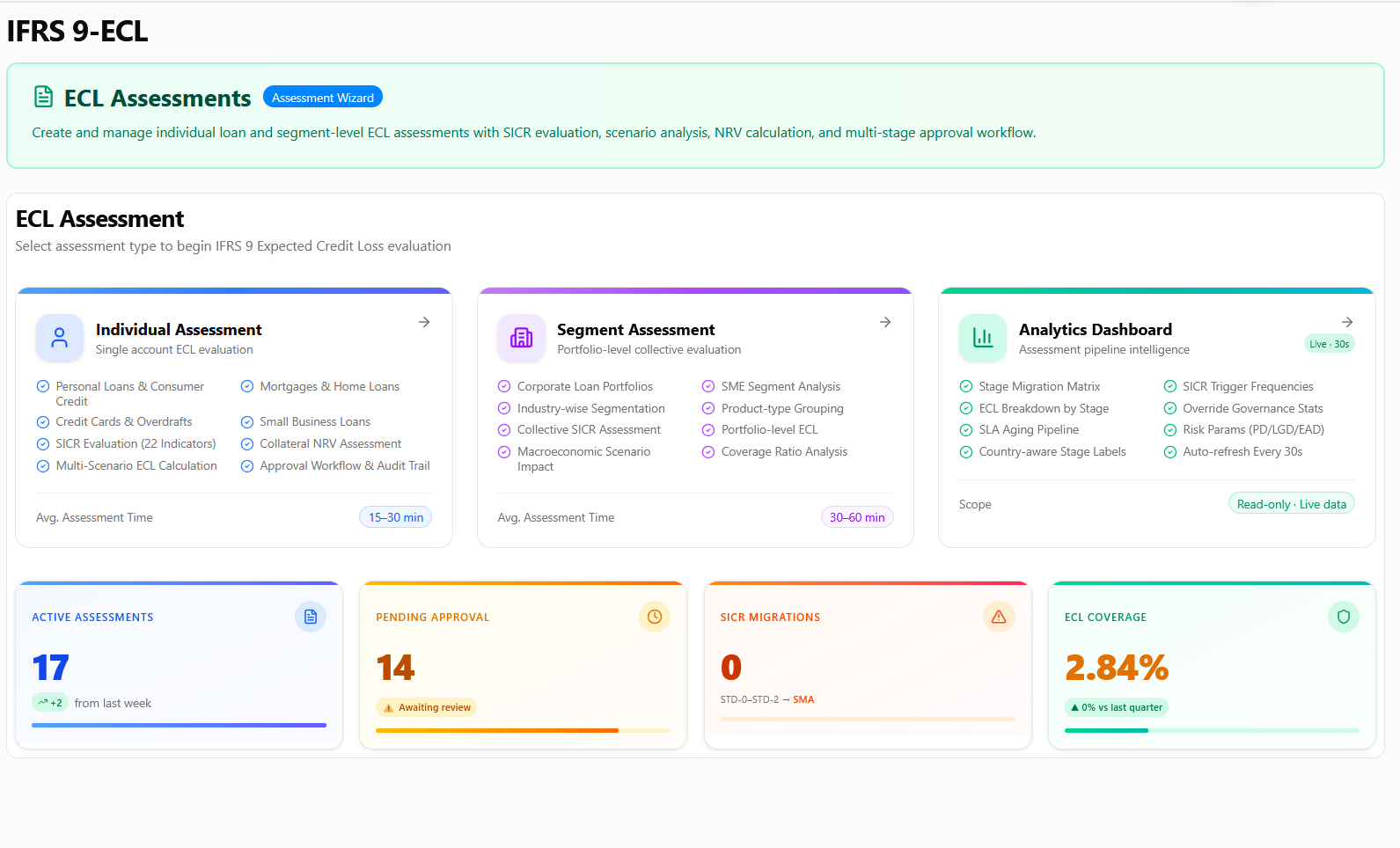

Portfolio Assessment

Guided 7-step wizard transforming raw CBS data into auditable risk parameters — from portfolio selection through ML-driven recommendations.

Portfolio Selection

Auto-populated loan data from Core Banking System — zero manual entry.

SICR Evaluation

Quantitative, qualitative, and jurisdiction indicators determine Significant Increase in Credit Risk.

Delay Analysis

Country-specific DPD thresholds aligned to IFRS 9 and local regulatory requirements.

Scenario Analysis

Multi-scenario probability-weighted ECL with World Bank, IMF, and central bank data.

NRV Collateral Assessment

Methodical collateral discount cascade producing defensible Net Realizable Value.

Regulatory Reports

Auto-generated CL-1 through CL-5 regulatory forms with EDW upload and 50+ templates.

Analytics & Audit Trails

Immutable audit trail, ML recommendations engine, and comprehensive ECL analytics.

Model Studio

Unified configuration workspace — develop, calibrate, and govern all risk parameters with 4-eye approval and version control.

PD Configuration

15 Model Methodologies

15 methodologies for estimating Probability of Default across rating grades and segments

- TTC vs PIT calibration methods

- 22-grade rating scale (S&P/Moody's/Fitch aligned)

- Term structure: constant hazard, Kaplan-Meier, Markov chain

Configuration Preview

+ 7 more methodologies

ECL Calculation Engine

Four calculation methodologies — from deterministic to stochastic — choose the right approach per portfolio segment and regulatory requirement.

Stage Distribution

Stage 1

65%

Stage 2

25%

Stage 3

10%

ECL Trend (6 Months)

Scenario Analysis

Probability-weighted ECL under IFRS 9 §5.5.17 with real-time macroeconomic data from World Bank, IMF, and central banks.

Live macroeconomic data streams from World Bank, IMF & central banks

Baseline

50% weightMost likely economic trajectory based on current forecasts

GDP

3.5%

Unemployment

5.2%

Interest

6.5%

Optimistic

25% weightFavorable conditions with accelerated growth

GDP

5.0%

Unemployment

3.8%

Interest

5.0%

Pessimistic

25% weightAdverse scenario with recessionary stress

GDP

1.2%

Unemployment

7.5%

Interest

8.5%

Global Data Integration

GRC Sphere integrates real-time macroeconomic data from World Bank, International Monetary Fund (IMF), and central bank statistical databases. GDP growth, unemployment rates, inflation trajectories, property price indices, and interest rate forecasts are automatically populated — ensuring forward-looking ECL assessments reflect the most current global and domestic economic outlook.

Regulatory Reports

Comprehensive regulatory reporting with auto-generated CL forms, EDW upload, CIB reporting, and 50+ pre-built templates.

Reporting Templates

CL Form Automation

CL-1 through CL-5 generated in seconds from CBS data.

EDW Upload

Batch management, validation, multi-channel delivery (FTP/SFTP), and submission history.

50+ Report Templates

Bangladesh Bank templates for capital adequacy, liquidity, large exposure, and migration.

Regulatory Frameworks

Built-in alignment with global accounting and regulatory standards

Expected credit loss accounting standard

International regulatory capital framework

Current expected credit loss methodology

Insurance contracts accounting standard

Jurisdiction-specific accounting principles

Central bank credit risk guidelines

Plus IAS 1, IAS 39, and additional local regulatory reporting frameworks

Industries We Serve

Tailored IFRS 9-ECL solutions for financial institutions, lenders, and regulated entities across diverse sectors.

Banking

IFRS 9 for Banking Portfolios

Banks must calculate expected credit losses across diverse loan portfolios under IFRS 9. IFRS 9-ECL provides ML-powered ECL modeling, multi-scenario SICR evaluation, stage classification, and 50+ regulatory report templates — supporting standard, simplified, Monte Carlo, and multi-period calculation methodologies.

Fintech

ECL for Digital Lending

Digital lenders need robust credit loss calculation for regulatory compliance and investor reporting. IFRS 9-ECL delivers automated ECL calculations, portfolio assessment workflows, and scenario analysis — helping fintech lenders meet IFRS 9 requirements with scalable credit risk infrastructure.

Insurance

IFRS 9 for Insurance Investments

Insurance companies with credit exposures must calculate expected credit losses on bonds and other debt instruments. IFRS 9-ECL provides dedicated ECL modeling for insurance portfolios, supporting the unique credit risk profiles and regulatory requirements of the insurance sector.

Capital Markets

IFRS 9 for Investment Portfolios

Capital markets firms managing credit-sensitive instruments require precise ECL calculations. IFRS 9-ECL delivers sophisticated credit loss modeling, Monte Carlo simulation, and multi-scenario analysis for trading books, bond portfolios, and structured credit products.

Portfolio-to-Audit workflow

Standard / Simplified / MC / Advanced

CL-1 to CL-5 • EDW ready

Global portfolio coverage

Why IFRS 9-ECL?

The platform that transforms ECL compliance from spreadsheet burden into automated precision

Automated ECL

PD × LGD × EAD with stage allocation, scenario weighting, and discount factor application.

Stage Migration

Real-time monitoring with SICR triggers, cure tracking, and multi-level approval workflows.

Model Studio

Full lifecycle management with calibration, backtesting, version control, and validation.

Scenario Engine

Probability-weighted ECL with live World Bank/IMF macro-economic data integration.

Dual Alignment

Simultaneous compliance with IFRS 9 international and local central bank requirements.

Audit Ready

Immutable audit trail, disclosure templates, and submission-ready regulatory reports.

Frequently Asked Questions

Everything you need to know about IFRS 9-ECL

ECL With Confidence

See IFRS 9-ECL in action. Schedule a demo and discover how to automate expected credit loss with precision and governance.